Best Provident Fund Scheme

This is a voluntary, fully funded, and privately managed pension scheme established under Ghana's National Pensions Act, 2008 (Act 766). It serves as a supplementary retirement savings plan, allowing both employers and employees in the formal sector to contribute additional funds beyond the mandatory Tier 1 and Tier 2 schemes. The scheme is administered by licensed corporate trustees, such as Standard Pensions Trust, and is designed to enhance retirement benefits and provide financial flexibility.

Contribution Limits & Tax Benefits

Tax Reliefs

Contributions up to 16.5% of an employee's monthly basic salary are tax-deductible, offering significant tax savings for both employers and employees.

Additional Contributions

While contributions beyond 16.5% are permitted, they do not attract tax reliefs.

Informal Sector

For workers in the informal sector, contributions up to 35% of declared income are eligible for tax exemptions.

Scheme Objectives & Benefits

Enhanced Retirement Savings: Augments retirement income by providing an additional savings avenue beyond mandatory schemes.

Tax Efficiency: Maximizes tax benefits through allowable deductions on contributions.

Lump Sum Payout: Offers a guaranteed lump sum payment upon retirement or after meeting specific conditions.

Financial Flexibility: Allows for early withdrawals under certain conditions, such as medical emergencies or mortgage financing.

Why Provident Fund Scheme?

Expert Fund Management

Managed by experienced professionals ensuring optimal returns on investments.

Regulatory Compliance

Fully licensed and regulated by the National Pensions Regulatory Authority (NPRA), ensuring transparency and security.

Customized Solutions

Tailored pension solutions to meet the unique needs of both employers and employees.

Digital Access

User-friendly online platforms for real-time access to account information and statements.

Nationwide Presence

Extensive branch network providing accessible support across the country.

Feature Overview

| Feature | Details |

|---|---|

| Voluntary Contributions | Up to 16.5% of basic salary (tax-deductible); higher contributions allowed without tax reliefs |

| Tax-Free Withdrawals | After a minimum of 10 years of continuous contribution |

| Early Withdrawal Options | Permitted under specific conditions, subject to applicable taxes |

| Professional Management | Funds managed by NPRA-licensed trustees and fund managers |

| Digital Services | Online portals and mobile access for account management |

| Portability | Funds are transferable when changing employment |

Eligibility & Access Conditions

Enrollment: Open to all employees in the formal sector. Enrollment can be initiated by either the employer or the employees through mutual agreement.

Withdrawal Conditions:

- Standard Withdrawal: Tax-free withdrawals permitted after 10 years of continuous contribution.

- Early Withdrawal: Allowed under certain conditions (e.g., medical emergencies, mortgage financing) but may be subject to a 15% tax on the withdrawn amount.

- Retirement: Full access to accumulated funds upon reaching the retirement age as defined by the scheme.

- Permanent Disability or Death: Immediate access to funds for the contributor or their beneficiaries.

Additional Notes

Regulatory Oversight: The scheme is governed by the NPRA, ensuring adherence to investment guidelines and protection of members' interests.

Investment Strategy: Funds are invested in a diversified portfolio, including government securities, equities, and other approved instruments, aiming for long-term growth.

Member Education: Regular workshops and seminars are conducted to educate members on pension planning and scheme benefits.

Ready to start saving for your future?

Enroll in the Personal Pension Scheme (Tier 3) today and take advantage of tax benefits and flexible savings options.

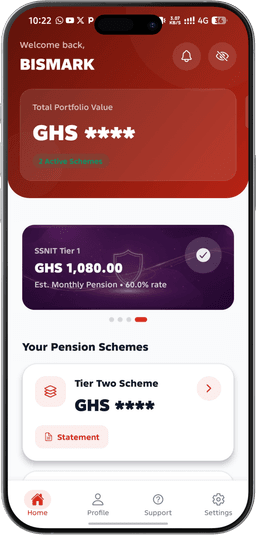

Manage your pension on the go

Track contributions, monitor fund performance, and access member services — all from your phone.